BlackFin Tech Weekly — February 27th

Every Monday, we publish a short digest which sums up last week's fintech activity.

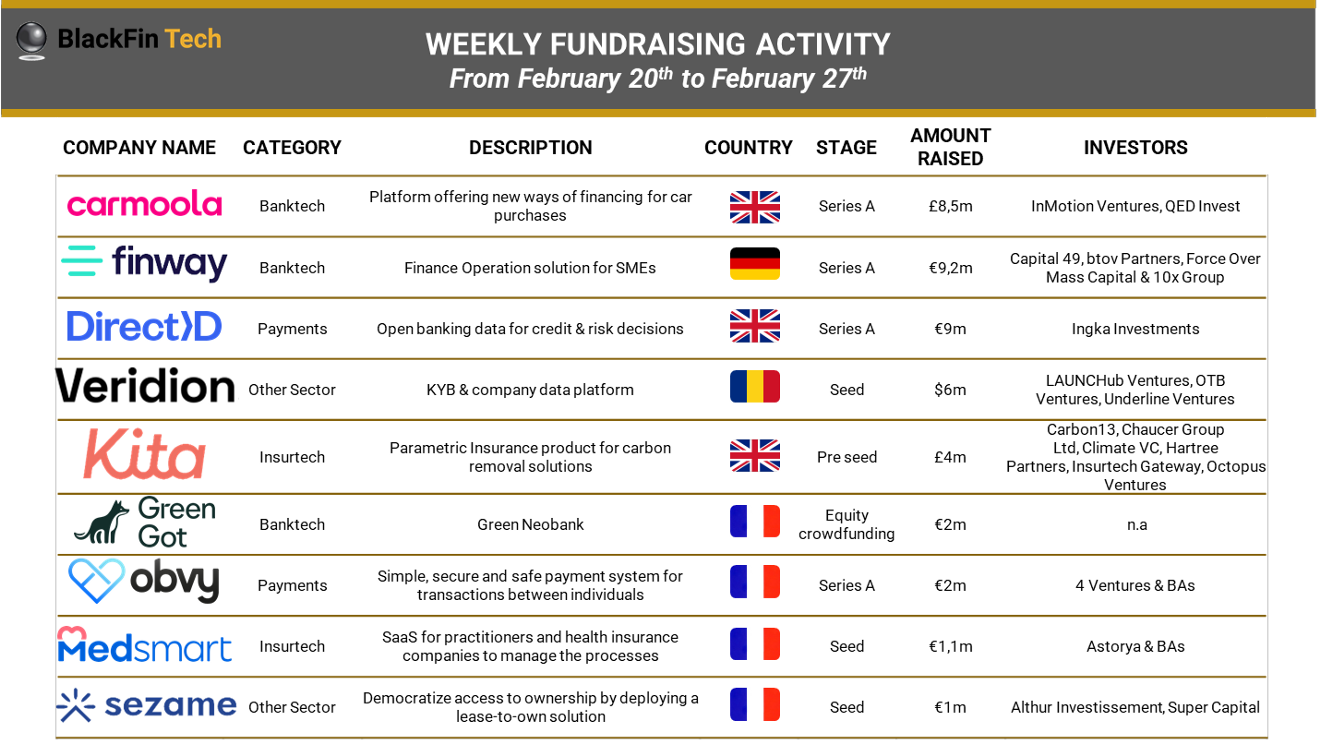

Dear Fintech folks, we hope you all had a great week. Temperatures cooled down again and so has the Fintech activity across Europe this week. Congrats to France for closing most deals and to the UK for raising the largest amounts.

Last week, a total amount of €42.7m was raised across 9 deals! Congratulations to British car financing platform carmoola in a £8.5m Series A followed by German finance operations solution finway in a €9.2m Series A. Finally, the British open banking data provider DirectID raised a €9m Series A.

France is occupying the first place with four deals this week, followed by the UK with three deals and Germany and Romania with one deal each.

Subsector-wise, most deals were in Banktech (3), followed by Payments, Insurtech and other sector each generating two deals.

Let’s dive in:

Carmoola raised £8.5m:

British Carmoola has raised a £8.5m Series A with InMotion Ventures, QED invest and a £95m debt facility.

Launched only ten months ago, Carmoola is liberating the archaic, slow, and backwards car finance market with a new, straightforward “neo car finance” product that is effortless to use and reduces the time taken to complete a car purchase from days to just minutes.

The funding will be deployed to continue scaling the business and support the rapid customer adoption Carmoola has seen since its launch. The plan is to grow the team to 20 people to meet demand, with the customer at the heart of their business.

Finway raised €9.2m:

Finway, the German finance operating system for SMBs, raised €9.2m in a Series A from Capital 49, an early stage venture fund led by founders of global fintech unicorn Airwallex.

Finway replaces the inefficient, fragmented SMB finance tool market with one centralized platform covering invoicing and accounting workflows, spend and travel expense management.

DirectID raised €9m:

DirectID raised €9m in a Series A round with IKEA operator Ingka Group’s investment wing.

The British Fintech risk platform enables informed credit and risk judgements by businesses. The platform relies on access to open banking data provided by 13,000+ partners, spread across 65 countries.

Congrats also to Veridion, Kita, Green Got, obvy, medsmart and sezame on their respective rounds.

In addition to the fundraising activity, we also observed a couple of M&A deals this week.

Doconomy, the climate tech that enables CO2 and H2O calculations for all digital financial transactions, has acquired Dreams Technology, the financial wellbeing fintech. The acquisition will enable Doconomy to offer clients an extended product portfolio that will include modules for climate smart savings, debt management, and investments.

Percayso Inform, the data intelligence provider, has acquired Cazana, a leading data insights platform for the European automotive industry. The unified data and intelligence hub will allow insurers, brokers, and MGAs to access aggregated data streams via API, with the option of integrating tailored strategies through rules-based parameters and models.

And here are the news that caught our eye last week, enjoy:

Stripe: Launch of Enhanced Issuer Network with a set of major US card issuers including Capital One and Discover + Tap to Pay on Android enabling businesses in six countries to accept contactless in-person payments using a compatible phone or tablet without the need for traditional point-of-sale hardware.

Pitchbook 2022 Annual European VC Valuations Report : Down rounds register lowest share in a decade. Overall, the median early-stage valuation registered a 23.4% year-over-year (YoY) increase, but the drop in Q4 suggests that investors weren’t as willing to pay the high premiums that were available to startups earlier in 2022. Down rounds fell to 15.2% of overall VC deals in 2022 despite worsening market conditions for European startups. This may be due to companies opting for more heavily structured funding rounds instead of taking a valuation cut, which often paints startups in a negative light. Down rounds are likely to increase in 2023 as cash reserves tighten.

F-Prime Capital released its annual State of Fintech Report

The F-Prime FinTech Index is designed to track the performance of emerging, publicly traded financial technology companies. It was down 72% for the year 2022 due to 3 reasons: the changing macro environment, public re-appraisal of fintech companies and some verticals’ exposure to credit cycles. Public market corrections are directly impacting private markets. All verticals have declined. Proptech has declined the most, with an 89% decrease of the average fintech index. Payment and B2B Saas were the least impacted.Coinbase beats on revenue and earnings, but usage continues to decline on Q4 2022. The crypto exchange reported a $629m in revenues, vs. $590m as expected by Refinitiv analysts. It is still a decrease of 75% YoY. Also, Coinbase’s user base continues to shrink. The company said it had 8.3m monthly transacting users (MTUs) during the fourth quarter, down from 8.5m the prior period.

Have a great week & see you next Monday!