H2 2023 FINTECH WRAP-UP 🌯

Discover Fintech Wrap-Up, a newsletter about all things Fintech & Insurtech in Europe, by BlackFin Tech.

Welcome back BlackFin Tech readers!

Here is our last newsletter of the year - admitting that these past few months have been intense is quite an understatement…

In July, we were writing about our commitment to “look at startups that had the ability to remain stable despite the chaotic environment”. Turning words into action, we invested in 3 new fintechs in the last quarter - every one of them embodying a deeply rooted trend.

But before telling you more, we thought it would be interesting to deeply look back at the global fintech data from 2023.

📊 WHAT SHAPED EUROPEAN FINTECH IN 2023

As we cozy up to the end of another year, we looked, once again, at our treasure trove of data. We've crunched the numbers and even consulted our fortune tellers… 🔮

Disclaimer: all data is as of the 15th of December.

In line with the VC market slowdown that began in 2022, European fintech-insurtech fundraising witnessed a decline in 2023, both in volume and value. While over 800 fundraising rounds occurred in 2022, only 650 secured funding in 2023. Notably, the total funds raised plummeted from nearly €17 billion in 2022 to €5.4 billion in 2023.

It’s worth noticing, however, that if we exclude high-value outliers (deals exceeding €100 million), the difference in funds raised in 2023 versus 2022 decreases from -67% (i.e. 11.6bn funding gap) to -52% (i.e. 5.9bn funding gap).

The 2022-2023 quarterly comparison paints a clear picture: 2022 signaled the impact of public market declines on venture capital (see Q3 and Q4 in particular), while 2023 reveals the full brunt of these consequences.

Despite this, if we take a look at F-Prime Fintech Index with a focus on 2023, it displays a clear re-acceleration in public global fintechs, outpacing indices like those for SaaS companies. With a 16% growth in the last 6 months and over 30% since the beginning of Q3 2023, there's a hopeful hint at a consequential private fintech market recovery in 2024.

The slowdown in fundraising is observed across all European geographies, none excluded. The United Kingdom continues to play a leading role for European fintechs, but it’s by far the most impacted geography both in terms of drop in € raised and number of deals announced.

Other geographies are also impacted, however, it seems the impact mostly comes from outlier rounds as the number of deals closed remains rather stable.

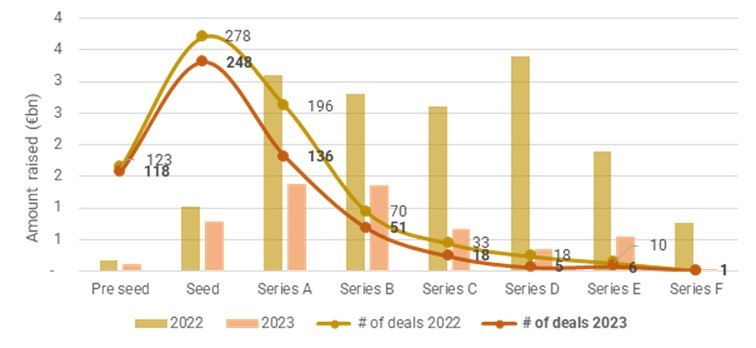

Analyzing transaction and investment data across various stages reveals a decline in both the number of deals and invested amounts, primarily attributed to later stage financing rounds (Series B and beyond). Pre-seed and seed stages appear to hold steady, maintaining a trajectory similar to that of 2022. This might suggest a potential revitalization in later-stage fundraising over the next 9 to 12 months.

During 2023, later-stage financing has seen more activity in the United Kingdom and Germany, with France, the 3rd major hub, slightly lagging.

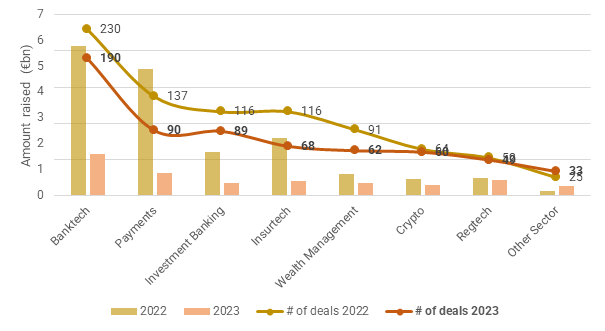

Within European fintech sectors, Banktech, Insurtech, and Payments are among the sub-sectors that are experiencing a more pronounced ‘downfall’.

In contrast, Regtech, possibly due to its reliance on ever-increasing European financial regulation (e.g., discussion around PSD3, new AML, etc), has attracted funds matching 2022 levels.

2023 has also been the year in which American investors refocused on their home country, being less present on the European scene. This is not unexpected as many heavyweights, like Tiger Global or Coatue, significantly slowed down their venture investment activity over the past year. A quite striking data point shows how US investors, during 2022, participated in nearly 60% of fintech fundraising in Europe vs 40% in 2023.

⭐ What are 2023’s 10 biggest rounds? ⭐

Out of the Top 10 deals, 8 are UK fintechs - which proves the relative strength of this ecosystem compared to its peers. The biggest round are mostly composed of Banktechs, Payments fintechs, Wealth management and Crypto - a sector that may be recovering after a tough winter.

🍳 WHAT WE SHAPED AT BLACKFIN TECH

Portfolio news

🇫🇷👋 In September, Akur8 raised another $25m and welcomed 2 new investors: FinTLV Ventures and Guidewire Software. What a journey since we first invested in the insurtech, back in early 2020!

🇬🇧💰 A few weeks later, we led Timeline’s £10m Series B, the leading British fintech platform dedicated to independent financial advisers (IFAs) which simultaneously reached an impressive £3 billion in Assets Under Management

🇳🇱💚 October was green for us, as we led Carbon Equity’s Series A. Carbon Equity is the world’s first platform to unlock access to climate venture capital and private equity. Looking forward to change the investment landscape with Jacqueline and her stellar team!

🇫🇷👯♂️ In November, we were proud of leading Indy’s Series C - the most-advanced AI-powered DIY bookkeeping & accounting software dedicated to freelance and independent workers

🇩🇪🏅 This year, our German champ Hawk:AI won the coveted Special Award for AI at the 2023 Fintech Germany Award. Congrats!

Team news

BlackFin is expanding: in Q4, we opened an office in Amsterdam! Come and say hi 👋

🔮 Coming soon… our predictions for 2024!

It’s both a tradition and a collective teamwork: with every new year come BlackFin Tech’s finest Fintech & Insurtech predictions.

This year, we asked you to vote for your favorite trend on Linkedin - if you haven’t done it yet, hurry up!

Thanks for reading, see you next year ✨